- 2025-10-31T00:00:00

- Company Research

VIC reported Q3 2025 NPAT-MI of VND640bn (USD25mn; -88% YoY and vs a net loss of VND941bn/USD36mn in Q2 2025), supported by (1) property handovers and bulk sales recognition, (2) continued positive EBIT of the hospitality segment, and (3) total divestment income of VND30.9tn (USD1.2bn), mainly from the completed transfer of Novatech to the Chairman (announced on August 14, 2025), which offset higher losses from the industrial segment.

For 9M 2025, VIC’s NPAT-MI was VND6.7tn (USD257mn; -31% YoY), mainly driven by (1) property handovers, (2) positive 9M EBIT from the hospitality segment, (3) the Novatech divestment gain in Q3 2025, (4) the Chairman’s grants to VinFast of VND23tn (USD885mn) in 9M 2025, and (5) transfer of the Global Gate project in Q1 2025 with a pre-tax profit of VND16.7tn (USD642mn), which more than offset (6) losses from the industrial segment and financial expenses.

VIC’s 9M 2025 NPAT-MI completes 52% of our full-year forecast. We foresee insignificant changes to our 2025F NPAT-MI forecast, pending a fuller review.

- Property segment: See more details in our October 30, VHM Earnings Flash.

- Hospitality segment: The segment’s EBIT in Q3 2025 was VND112bn (USD4mn), continuing the positive trend since turning around in Q2 2025 at VND185bn (USD7mn). The segment’s 9M 2025 EBIT was positive at VND65bn (USD2.5mn) vs a 9M 2024 EBIT loss of VND822bn (USD32mn).

- Industrial segment:

- Delivery results: In Q3 2025, VinFast delivered 38,195 EV cars globally (+7% QoQ) and 120,052 e-scooters (+73% QoQ).

- For 9M 2025, VinFast’s global EV car deliveries totaled 110,362 units (vs the FY2024 result of 97,400 cars; 73% of our full-year forecast), with Vietnam accounting for 94% of the volume. E-scooter deliveries reached 234,536 units (vs the FY2024 result of 71,000 units; exceeding our full-year forecast).

- The segment reported EBIT loss margin at -103% in Q3 2025 (38,195 EVs delivered) vs -71% in Q2 2025 (35,837 EVs) and –83% in Q1 2025 (36,330 EVs).

- Capital support from Chairman to VinFast:

- Novatech transfer: In August 2025, VinFast announced plans to spin off certain completed R&D assets into new company Novatech and transfer its stake in Novatech to VIC’s Chairman for VND39.8tn (USD1.5bn). The transfer was completed in Q3 2025 and was a major contributor to VIC’s divestment income during the quarter.

- Grants from Chairman to VinFast: Following the November 2024 announcement of a new capital support agreement – comprising up to VND50tn (USD1.9bn) in grants from VIC’s Chairman to VinFast through 2026G – as of end-Q3 2025, VIC’s Chairman had disbursed cumulative grants of VND28tn (USD1.1bn) to VinFast. The disbursements included VND5.2tn (USD200mn) in Q4 2024, VND5.0tn (USD192mn) in Q1 2025, VND18tn (USD692mn) in Q2 2025, and no new disbursement in Q3 2025.

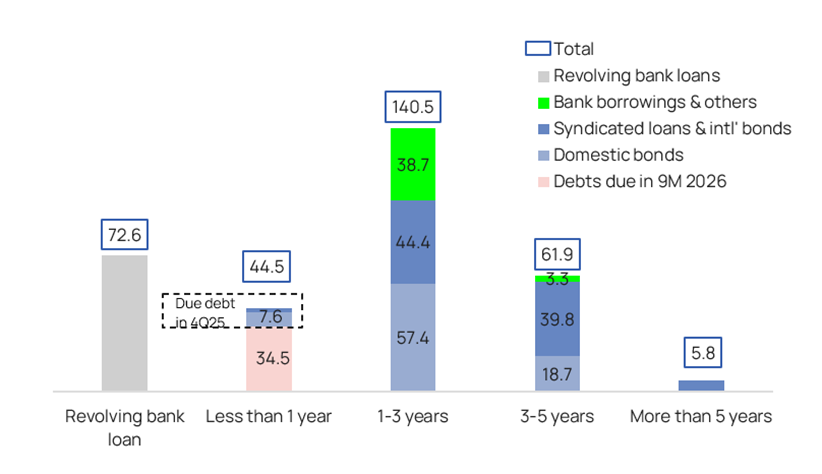

- Debt balance: As of end-Q3 2025, VIC’s total debt was VND325tn (USD12.5bn; +43% vs end-2024 and +15% QoQ), with unhedged USD-denominated debts accounting for 17.2% of the total debt. Debts maturing within 12 months include (1) revolving bank loans of VND72.6tn (USD2.8bn), (2) debts due in Q4 2025 amounting to VND10.0tn (USD386mn; in which domestic bonds of VND7.6tn/USD292mn, syndicated loans and international bonds of VND2.0tn/USD77mn), and (3) debts due in 9M 2026 of VND34.4tn (USD1.3bn).

Figure 1: VIC’s 9M 2025 results

VND bn | 9M | 9M | % YoY Growth | 2025F | 9M as % | Vietcap’s comments on 9M 2025 results |

Net revenue | 126,916 | 169,611 | 34% | 293,813 | 58% |

|

| 65,260 | 78,291 | 20% | 167,710 | 47% | * Mainly driven by 1) handovers at Royal Island and Ocean Park 2&3, and 2) the transfer of the Global Gate project in Q1 2025 with revenue of VND43.5tn/USD1.7bn and pre-tax profit of VND16.7tn/USD642mn. |

| 6,482 | 8,390 | 29% | 11,119 | 75% | * YoY growth was driven by both the hotel and amusement park segments. |

| 28,142 | 50,657 | 80% | 81,495 | 62% | * VinFast's global EV deliveries in 9M 2025 totaled 110,362 units (with Vietnam accounting for 94%), completing 73% of our 2025F delivery forecast. |

| 27,032 | 32,273 | 19% | 33,490 | 96% | * Mainly from construction services. |

|

|

|

|

|

| |

EBIT | -4,291 | -13,290 | N.M. | 24,863 | N.M. |

|

| 20,717 | 25,203 | 22% | 63,140 | 40% |

|

| -822 | 65 | N.M. | 357 | 18% | * Quarterly EBIT in Q3 2025 was VND112bn (USD4mn), continuing the positive trend since turning around in Q2 2025 at VND185bn (USD7mn). |

| -28,014 | -43,594 | N.M. | -42,628 | 102% | * The segment’s EBIT loss margin was -103% in Q3 2025, vs -71% in Q2 2025 and –83% in Q1 2025. |

| 3,827 | 5,036 | N.M. | 3,994 | 126% |

|

|

|

|

|

|

|

|

Financial income | 37,813 | 39,894 | 6% | 9,750 | 409% | * Includes: (1) a divestment gain from the Novatech transfer in Q3 2025; (2) recognition of bulk sales at Golden City with a pre-tax gain of VND3.5tn (USD135mn) in Q3 2025; and (3) a partial divestment of VinAI’s business to Qualcomm with a pre-tax gain of VND1.8tn (USD68mn) in Q1 2025. |

Financial expenses | -23,493 | -31,308 | 33% | -33,318 | 94% |

|

Profit from associates | 686 | 529 | N.M. | 827 | 64% |

|

Other gain (loss) | 577 | 19,359 | N.M. | 18,000 | 108% | * Includes the Chairman’s grants to VinFast amounting to VND23tn (USD885mn) in 9M 2025 (with VND5.0tn/USD192mn in Q1 2025 and VND18tn/USD692mn in Q2 2025, and no new disbursement in Q3 2025). |

PBT | 11,292 | 15,183 | 34% | 20,122 | 75% |

|

Tax expenses | -7,223 | -7,618 | 5% | -10,118 | 75% |

|

PAT | 4,069 | 7,565 | 86% | 10,004 | 76% |

|

Minority interest | -5,642 | 887 | -116% | -2,904 | -31% |

|

NPAT-MI | 9,711 | 6,678 | -31% | 12,907 | 52% | * 9M 2025 NPAT-MI was mainly supported by 1) property handovers and bulk sales recognition, 2) positive 9M EBIT for the hospitality segment, 3) the Novatech divestment gain in Q3 2025, 4) the Chairman’s grants to VinFast in 9M 2025, and 5) transfer of the Global Gate project in Q1 2025. |

|

|

|

|

|

|

|

EBIT margin | -3.4% | -7.8% |

| 8.5% |

|

|

| 32% | 32% |

| 38% |

|

|

| -13% | 1% |

| 3% |

|

|

| -100% | -86% |

| -52% |

|

|

|

|

|

|

|

|

|

PBT margin | 8.9% | 9.0% |

| 6.8% |

|

|

PAT margin | 3.2% | 4.5% |

| 3.4% |

|

|

Effective tax rate | 64.0% | 50.2% |

| 50.3% |

|

|

NPAT-MI margin | 7.7% | 3.9% |

| 4.4% |

|

|

Source: VIC’s consolidated financial statements, Vietcap forecasts (updated August 29, 2025)

Figure 2: VIC’s total debt breakdown by maturity (VND tn) as of end-Q3 2025

Source: VIC, Vietcap compilation

Powered by Froala Editor